One of the most common questions I get asked is about investing. How should I start investing? What investment options do you recommend? What is a low-risk investing option? Don’t worry, we’re going to get there. But first, let’s start with something more basic.

Investing is a means to an end, not an end itself

Understanding how stocks and bonds work is pretty cut and dry, but the context matters – and in this case, the context is your financial situation and goals. I want you to start by going back to your “why.” What concrete financial goals do you have for your future?

Your goal could be buying a home, paying for your children or grandchildren to go to college, retiring at a certain age, or saving up to start your own business. Once you know this goal, you can figure out how much money you will need to accomplish it and when you will need this money.

Do you have your “why” ready? Let’s dive in!

What are stocks?

When you buy a stock, you are investing in a company. If the company grows and the stock becomes more valuable, your investment will grow with it. However, if the company fails or becomes less valuable (which happens to companies every day), your stock could be worth less or even nothing.

What are bonds?

When you buy a bond, you are loaning money to a company. The company will then repay your loan with interest at a specific time. The company may also pay you dividends (a percentage of the company’s earnings). Bonds are generally considered “safer” investments than stocks – less likely to lose all their value, but also less likely to increase hugely in value.

What is your risk tolerance?

The stock market as a whole goes up and down regularly. Sometimes it seems to go up, up, and up, and sometimes it plunges down. From 2000 to 2002, for example, the U.S. stock market lost about half of its value. Most investors agree that a big drop is inevitable at some point. So how willing are you to take on that risk? You have to think about the upside AND the downside when choosing to invest.

Creating your portfolio

So there are different types of investments, and those investments carry different levels of risks.

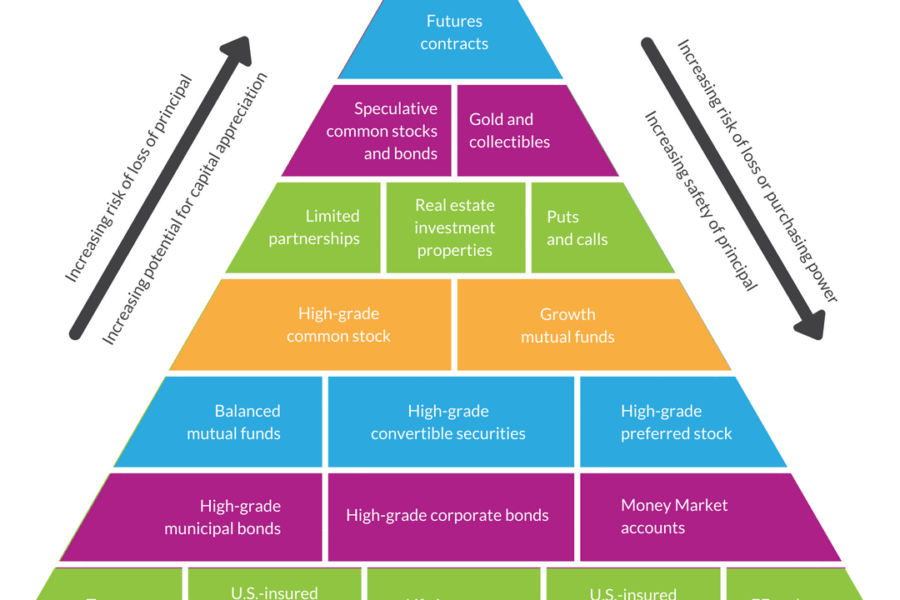

This image is modified from Smart About Money’s “Determining Your Risk Tolerance” lesson.

Depending on your risk tolerance, you can fill your portfolio with an allocation of risky and safe assets that matches your preferences. Your portfolio should be part of your overall financial plan so take into consideration the status of your savings and ability to weather changes in the economy.

Remember that the “safer” investments carry a different kind of risk, which investors call inflation risk. This is the risk that, over time, your money will have less buying power due to inflation. In the short run, you don’t have to worry much about inflation; but over decades, inflation will significantly impact the buying power of your money if you keep that money in safe investment vehicles like cash.

Investing is just one piece of the puzzle

I hope you see that investing is not an end in itself. Whether you keep your money in cash or in the stock market, you are taking on certain risks. Remember to view investing as just one piece of your financial life and align it with your short- and long-term goals. While looking into investing, make sure you’re taking care of yourself by maintaining an emergency fund and protecting your important assets.

My perspective on investing is inspired by a great resource called Transparent Investing. I hope you check out the full guide if you’re interested in learning more. All of the information here is for educational purposes and I encourage you to only take investment advice from a Certified Financial Planner® or another investment professional.

This image is modified from Smart About Money’s “Determining Your Risk Tolerance” lesson.

Depending on your risk tolerance, you can fill your portfolio with an allocation of risky and safe assets that matches your preferences. Your portfolio should be part of your overall financial plan so take into consideration the status of your savings and ability to weather changes in the economy.

Remember that the “safer” investments carry a different kind of risk, which investors call inflation risk. This is the risk that, over time, your money will have less buying power due to inflation. In the short run, you don’t have to worry much about inflation; but over decades, inflation will significantly impact the buying power of your money if you keep that money in safe investment vehicles like cash.

This image is modified from Smart About Money’s “Determining Your Risk Tolerance” lesson.

Depending on your risk tolerance, you can fill your portfolio with an allocation of risky and safe assets that matches your preferences. Your portfolio should be part of your overall financial plan so take into consideration the status of your savings and ability to weather changes in the economy.

Remember that the “safer” investments carry a different kind of risk, which investors call inflation risk. This is the risk that, over time, your money will have less buying power due to inflation. In the short run, you don’t have to worry much about inflation; but over decades, inflation will significantly impact the buying power of your money if you keep that money in safe investment vehicles like cash.

{kind=link}