How do you balance debt and savings? Here’s what our research found.

If you’re paying down debt, saving money may be a low priority for you. After all, you’re probably paying interest on your debt every month, so paying off your debt more quickly means keeping more money in your pocket long-term.

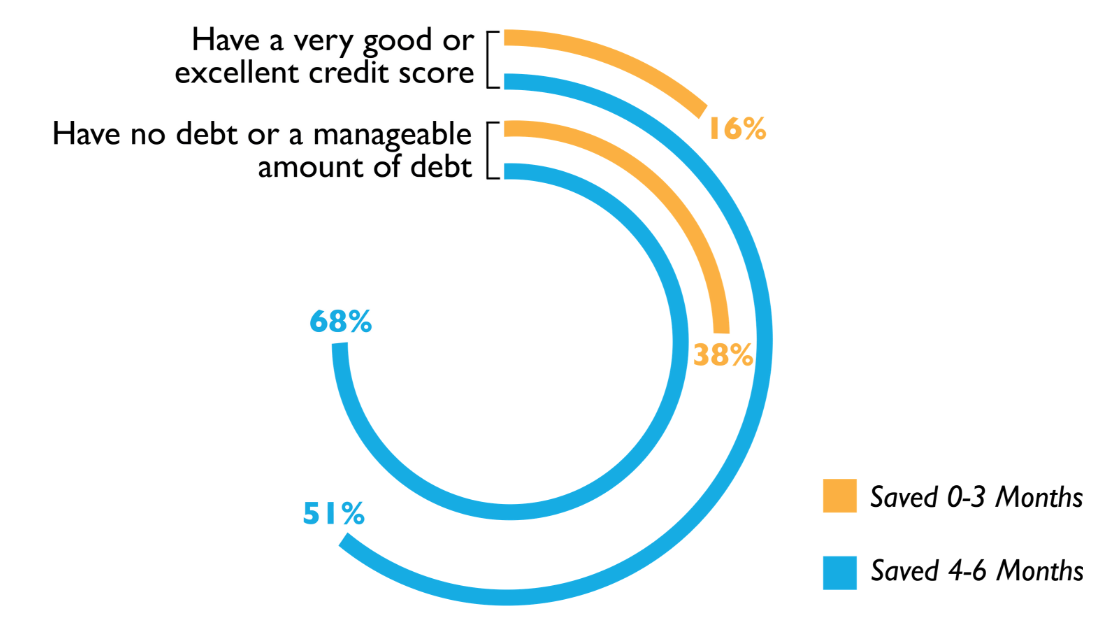

It’s harder to save when you have debt

Our research found that Savers with a very good or excellent credit score (the two highest categories) were more likely to save at least $20/month than Savers with lower credit scores. Savers who had no debt or a manageable amount of debt were also more likely to save.

What do the experts say?

Many experts believe that maintaining or building a small emergency fund is crucial even if you have debt. SaverLife’s Financial Coach Saundra Davis agrees. She says many people ask her, “Should I save or pay down my debt?” Her recommendation is a balanced approach. Focus on paying down debt, but don’t eliminate saving entirely.

Julia is part of EARN's Research and Innovation Team. If you join SaverLife, you may get emails from Julia asking you to help with our research. These are always optional (and you can unsubscribe at any time), but your voice helps us improve SaverLife and understand how we can better serve our members.