It’s in the news all the time: a record number of Americans have incomes that go up and down throughout the year. Some of these people work in the “gig economy,” driving for rideshare services like Lyft and Uber; some work seasonal construction jobs; and some perform childcare or freelance work when they can get it.

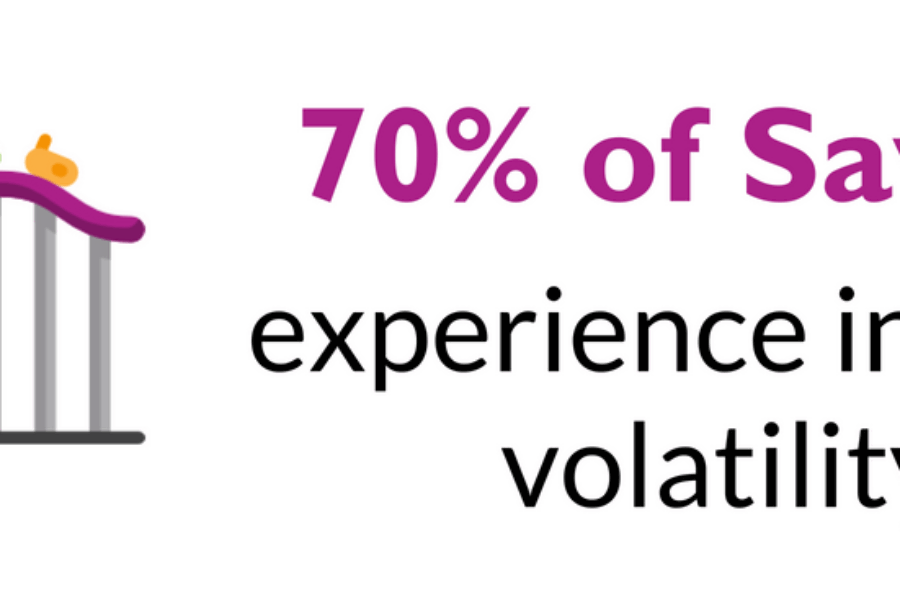

EARN’s research shows that SaverLife members have fluctuating incomes as well: 70% of Savers experience income volatility.

When you don’t know what your income is going to be every month, that can make it hard to plan and hard to save. We asked some of you: how do you deal with ups and downs in your income?

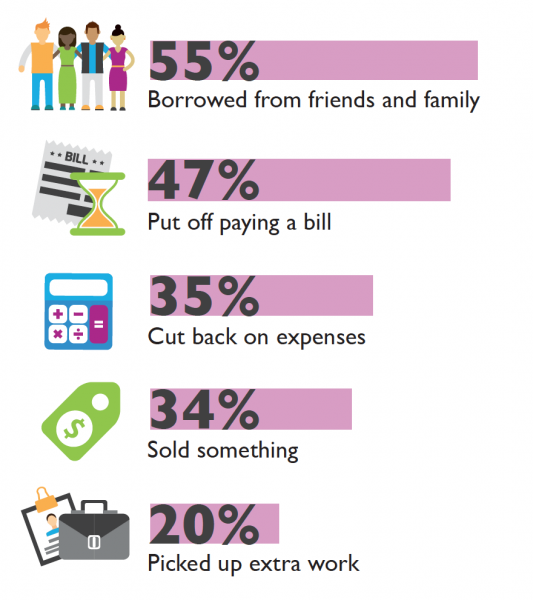

How Savers manage in times of lower income

Gabriella, a Saver from California, told us, “In a low period of income, we count on my girls or borrow from my parents. In a high period, we set aside money as savings, but something always comes up and we have to use it.”

Gabriella, a Saver from California, told us, “In a low period of income, we count on my girls or borrow from my parents. In a high period, we set aside money as savings, but something always comes up and we have to use it.”

Gabriella, a Saver from California, told us, “In a low period of income, we count on my girls or borrow from my parents. In a high period, we set aside money as savings, but something always comes up and we have to use it.”

{kind=link}